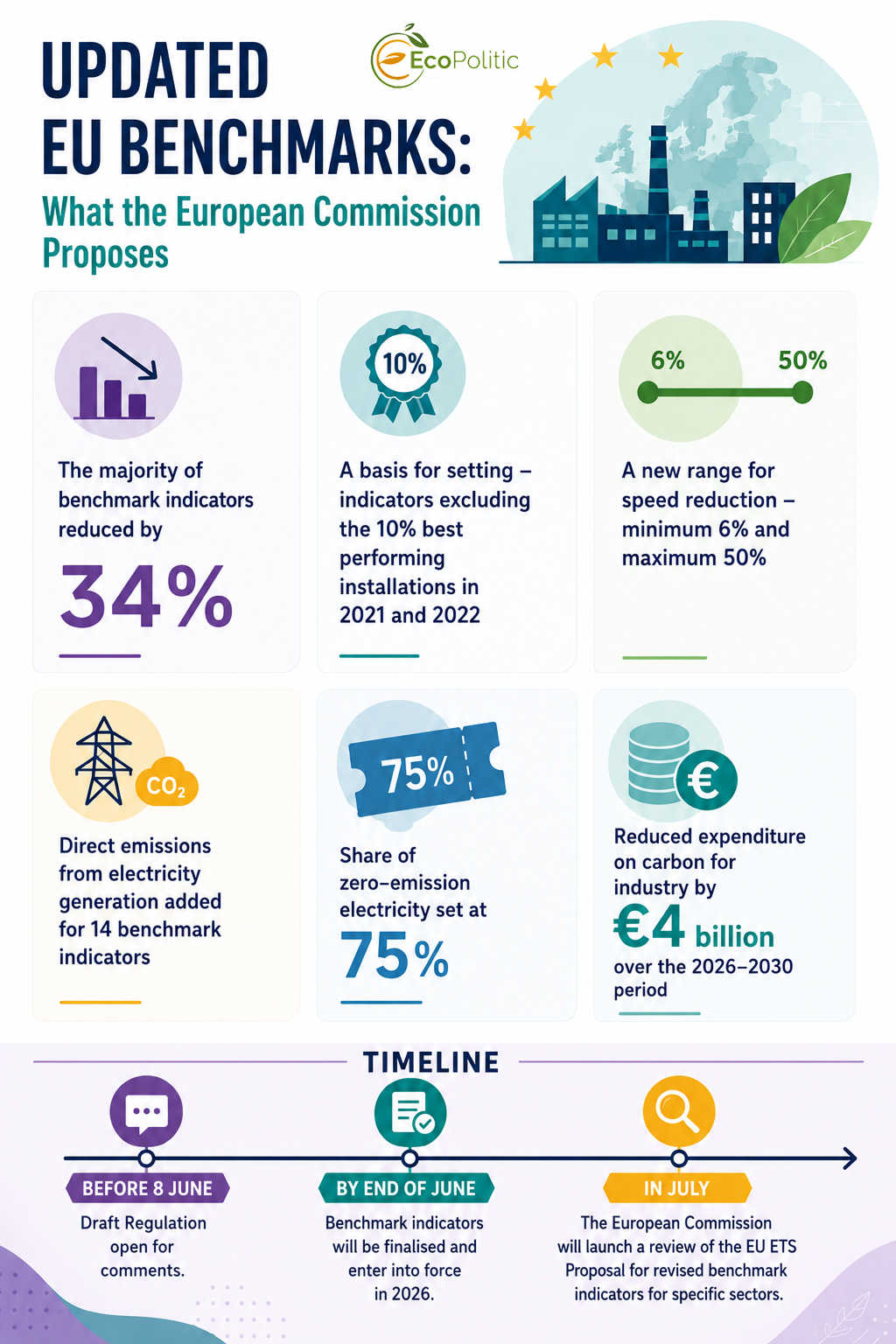

On May 11, the European Commission released for public consultation the updated benchmarks for the European Union’s Emissions Trading System (EU ETS), which will apply from 2026 to 2030. Stakeholders have been eagerly awaiting these figures, as they will, in particular, influence the allocation of free allowances and the cost of CBAM certificates.

EcoPolitic has gathered expert opinions on this European Commission proposal.

Why are the benchmarks receiving so much attention?

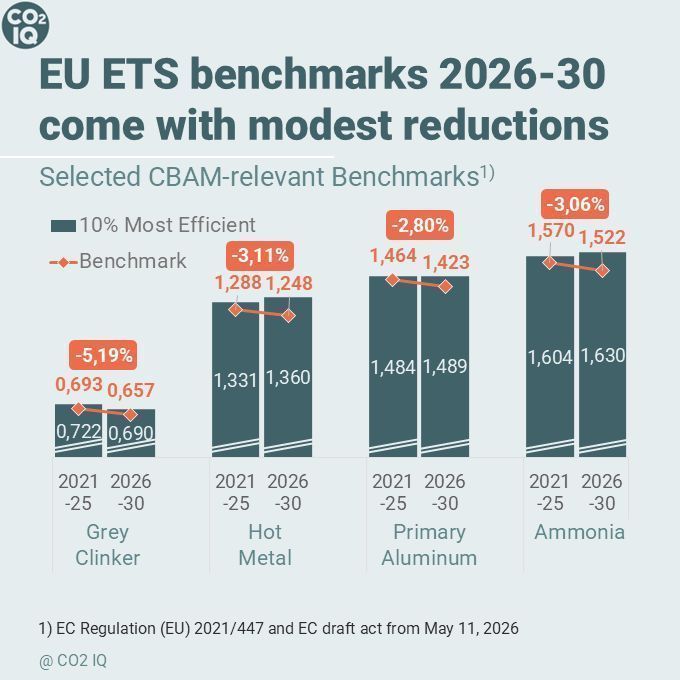

A benchmark is a reference level of emissions for a specific product or process. For example, for the production of 1 ton of steel, 1 MWh of electricity, 1 ton of cement, and so on.

Companies that operate more efficiently than the benchmark receive greater benefits, as they have enough free allowances and can even sell the surplus. Those who emit more CO₂ are forced to purchase additional allowances and invest in modernization.

Benchmarks determine how many free CO₂ emission allowances companies receive under the ETS. They also directly influence the “free allocation adjustment” for goods subject to the CBAM.

These EU ETS benchmark indicators are usually based on the emissions levels of the 10% most efficient installations in the EU. Even minor changes can significantly impact financial risks associated with carbon emissions.

What EU officials propose

The draft regulation published for consultation provides for adjustments to the calculations affecting the benchmark levels:

-

The vast majority of benchmark indicators have been significantly reduced – by about 34%. These very benchmarks will be adopted for use in the UK Emissions Trading System (UK ETS) and will determine the volume of free quota allocation for the period from 2028 to 2030.

Джерело: CO2 IQ, LinkedIn

-

The proposed benchmarks are based on the emissions levels of the 10% best installations in 2021 and 2022.

-

A new reduction corridor (minimum 6% and maximum 50%) is introduced, which applies over a 20-year period.

-

Indirect emissions from electricity have been added to 14 product benchmarks.

-

Overall, higher benchmark indicators maintain the number of free allowances at approximately 75% of industrial emissions – which will reduce carbon costs by about €4 billion during 2026–2030.

Timeline

-

The draft regulation is open for comments until June 8.

-

By the end of June, the benchmarks should be adopted and will enter into force starting in 2026.

-

In July, there will be a review of the EU ETS with a proposal on reserve benchmarks for specific sectors.

Expert opinions

The publication of new EU ETS benchmarks has sparked an active discussion among analysts, market participants, and climate policy experts. While most specialists acknowledge the need to adapt the system to new economic realities, assessments of the proposed changes vary significantly-from support for a more flexible approach to concerns about the risk of weakening the ETS mechanism itself.

Caution and a measured approach

Markus Ferdinand, Chief Analyst at Veyt, believes that the discussion around the new ETS parameters should not begin with a mechanical redistribution of quotas, but with defining the overall "carbon budget" that will align with the EU’s climate goals through 2040. In his view, the market requires a clear and consistent logic: first, the permissible emissions volume must be determined, and only then-the role of international quotas, flexibility mechanisms, and stability reserves.

The expert notes that as the market gradually contracts, the Market Stability Reserve (MSR) is increasingly becoming not only a stabilisation tool but also a liquidity support mechanism. Therefore, in his opinion, the EU should approach changes to the system more cautiously and avoid ad hoc decisions that could undermine investor confidence.

“The goal should not be to redesign the ETS, but to equip the existing system with a consistent logic for emission reduction and reliable flexibility instruments,” the expert emphasises.

A similar view is shared by Robert Jeszke, CEO of the Polish National Centre for Emissions Management. He believes that Europe is entering a new phase of climate policy, where the main challenge is no longer technically adjusting individual ETS parameters, but instead managing decarbonisation under economic and geopolitical pressures.

According to the expert, discussions regarding the ETS, CBAM, MSR, and industrial decarbonisation are increasingly converging on a fundamental question: can Europe build a climate system that is environmentally ambitious, economically viable, and politically resilient at the same time.

The expert compares the current situation to a Formula 1 race on a mountain road. Previously, the EU mainly focused on “engine power”-strengthening quota scarcity and raising the carbon price-but now “steering” and political legitimacy of the climate transition are becoming equally important.

Pragmatic attitude

At the same time, some experts interpret the new benchmarks as a sign of a more pragmatic approach by the European Commission to industrial policy. Georgi Gushlekov, a sustainability specialist at Dormakaba, notes that including indirect emissions in the calculation of free allowances could substantially reduce costs for energy-intensive sectors-especially the metallurgical, cement, and chemical industries.

На his view, this reflects a deeper dilemma in European climate policy: how to combine ambitious decarbonization targets with the need to maintain industrial competitiveness amid high energy prices and weak economic growth.

The expert cautions that additional flexibility in the system could have a double effect. On one hand, lower carbon costs could ease financial pressure on enterprises and provide them with time for modernization. On the other hand, excessive easing of the ETS risks weakening the investment signal needed for the development of low-carbon technologies.

“Competitiveness and decarbonization should not be viewed as conflicting objectives,” he emphasizes.

Radical proposals

Environmental think tanks are especially vocal against potential ETS weakening. In its study, the Öko-Institut warns that the debate about quota shortages and market liquidity could lead to an excessive increase in the supply of emission allowances.

The institute’s analysts believe that even under current rules, the system will already have a sufficient number of allowances to achieve the European Union’s climate goals by 2040. If, however, the EU further relaxes the linear reduction factor (LRF) or softens MSR mechanisms, this could result in a structural quota surplus.

According to the study’s authors, such a scenario poses a serious risk to the very logic of the ETS, since quota oversupply weakens the CO₂ price signal and reduces incentives for decarbonization investments.

Taking an even harsher stance, the international organization Carbon Market Watch in its report “Don’t mess with the ETS” directly criticizes attempts to increase free quota allocations or cap emission costs, calling this a threat to the system’s environmental effectiveness.

In the authors’ opinion, the ETS has already proven its effectiveness as an emission reduction tool and now must remain a strict mechanism to drive industrial transformation. Carbon Market Watch advocates for a faster phase-out of free allocation, strengthening the role of the Carbon Border Adjustment Mechanism (CBAM), and maintaining a robust Market Stability Reserve system.

The organization also emphasizes that the ETS should serve not only as a climate instrument, but also as an industrial one-stimulating electrification, the development of clean technology, and investments in low-carbon production.

Thus, the discussion around new EU ETS benchmarks now goes far beyond a technical review of indicators and formulas. It highlights an ever-deepening conflict between two approaches: the drive to protect the competitiveness of European industry versus the need to preserve a strong climate signal to ensure decarbonization of the EU economy.