There is a widespread belief that Ukraine should follow Europe's lead in everything on its path to EU membership: adopting existing policies, approaches, and regulatory instruments. However, mindless copying can not only be an inefficient waste of time and resources, but also deal a real blow to Ukraine's economy.

Today, EcoPolitic decided to figure out what Ukraine should adopt from European experience in the field of environmental taxation and what innovations would only do harm.

When environmental taxation was first introduced in the world

Finland was the pioneer in introducing a carbon tax in 1990. It was followed by Norway and Sweden (both in 1991), and later by Denmark (1994). These countries also introduced the first taxes and fees for other air pollutants, especially sulfur dioxide and nitrogen oxide emissions.

Greenhouse gases – separately

Since 2005, the EU has implemented a fundamentally new approach – the Emissions Trading System (ETS or EU ETS) began operating in the bloc. Its focus is greenhouse gases. Since then, the ETS has been introduced gradually, in several phases.

How it works: the government sets emission limits, and enterprises receive allowances for these emissions either for free or by purchasing them. If a plant emits fewer greenhouse gases than its allowances cover, it can sell the surplus allowances to another plant and receive additional income.

Unlike Ukrainian enterprises, European businesses do not pay the full cost of carbon emissions, but only for the portion not covered by free allowances.

Before the start of the current fourth phase, it was common in the EU for some enterprises to pay nothing for carbon emissions, as they had excess allowances.

Even after 20 years of improvements, challenges remain

In mid-February at the European Industry Summit in Antwerp, President of the European Commission Ursula von der Leyen and German Federal Chancellor Friedrich Merz publicly expressed diametrically opposed views regarding the functioning of the EU ETS. The former defended it, while the latter was quite critical.

A coalition of 13 EU countries is already preparing an appeal to the European Commission demanding a significant revision of the system. They believe that the EU ETS creates unprecedented pressure on European industry and deprives it of competitiveness.

According to European leaders, revenues from the sale of allowances were largely not spent on decarbonization and did not facilitate the “green” transition – which contradicts the main objective of the European ETS. This point is also indirectly echoed in official materials from the European Commission.

Environmental payments: the foundation of the European system

In the EU, environmental taxes are a broader concept than in Ukraine, as Ukrainian and European taxation systems operate on fundamentally different principles.

According to Regulation (EU) No 691/2011, an environmental tax is a tax whose tax base is a physical unit (or its proxy) of something that has a proven, specific negative impact on the environment.

Europeans distinguish four main categories of environmental taxes:

- energy taxes;

- transport taxes;

- pollution taxes;

- resource taxes.

The EU explicitly declares two main objectives for introducing such charges:

- to encourage more sustainable behavior of businesses and households based on the “polluter pays” principle;

- to generate revenues to address environmental damage.

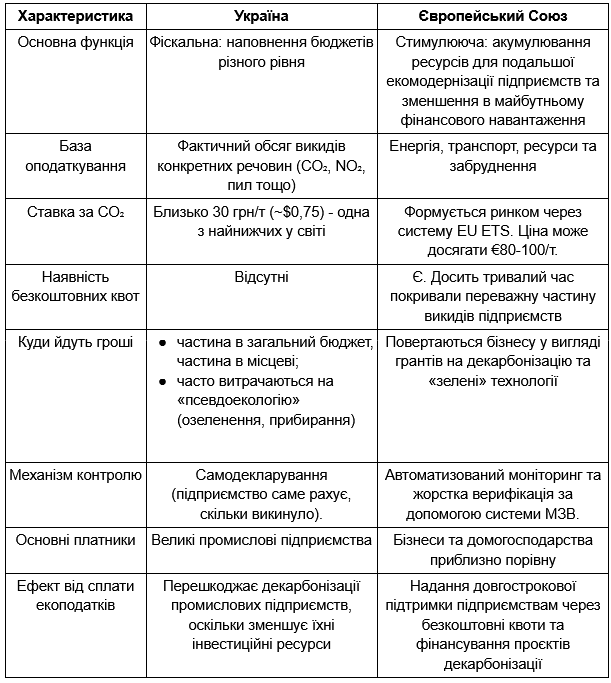

Ukraine and the EU: comparison of environmental taxation systems

The system established in Ukraine has a number of fundamental differences from the European one. These are presented in the comparative table below.

The Head of the Committee for Industrial Ecology and Sustainable Development of the European Business Association, Stanislav Zinchenko, says that an active discussion on eco-tax reform has been ongoing for the past seven years.

“The reform process itself and its effectiveness remain in question. I recall that a few years ago there were more than seven draft laws on eco-tax reform simultaneously,” the expert recalls.

Why can't Ukraine implement the European model right now?

The main reasons lie not in the environmental sphere, but are determined by economic laws and the realities of the full-scale war.

1. Risk of industrial collapse

If Ukraine suddenly introduced the European price for CO₂ emissions (for example, €80 per tonne), the production cost of Ukrainian steel and cement would rise dramatically. In wartime, when logistics are already expensive and plants are damaged, this would lead to the closure of key exporters. In addition, Ukrainian producers do not have free emission quotas like their European counterparts.

Farmers and ordinary citizens would also suffer financially due to a significant increase in the cost of fertilizers and electricity. Why so? In Ukraine, 80% of carbon taxes are paid by energy sector enterprises. Higher electricity prices will cause a chain reaction, raising the prices of all goods and services.

2. Lack of mechanisms for targeted reimbursement of funds

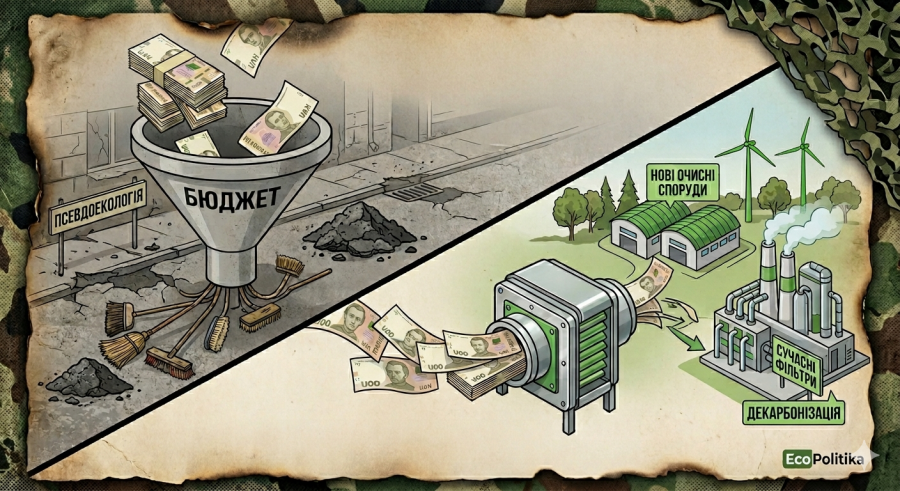

The European Union operates by the principle: “You pay a lot, but we give you back the same money for new filters.” In Ukraine, the lion's share of money from the environmental tax disperses across budgets at various levels. Business representatives say: “We are willing to pay more if this money does not go to patching budget holes but rather towards our own modernization.”

However, there is currently no mechanism for such targeted reimbursement. The hopes pinned on the Decarbonisation Fund of Ukraine have not materialized: proceeds from CO₂ emission payments are mainly directed at energy efficiency projects for government agencies and communities, not at decarbonizing the main greenhouse gas emitters.

3. Monitoring issue

The European system is based on accurate figures. In Ukraine, a significant portion of emissions is still calculated on paper and by visual estimates, using methodologies from the 1990s.

Furthermore, with the onset of full-scale invasion, the system for monitoring, reporting, and verification of greenhouse gas emissions was suspended. Deputies of the Verkhovna Rada only voted to restore it at the beginning of 2025. The law required enterprises to submit reports for 2024, but allowed them more time to prepare the documentation. Instead of March 31, the deadline was set by deputies as December 31.

4. The war factor

The majority of Ukrainian polluters are thermal power plants and metallurgical plants that are under constant shelling. Demanding that a company, which operates on generators or is under constant attack, pay high environmental taxes at European rates means halting the operations of these industries.

Companies are forced to spend part of their financial resources on restoring capacity instead of upgrading equipment. In addition, under current conditions, they cannot attract external financing on preferential terms.

5. Higher energy and carbon intensity of production compared to the EU

The reasons are structural:

-

a significant part of the metallurgy and energy sectors operates on 1980s–1990s equipment;

-

there is a large share of thermal generation (coal, gas) in Ukraine, while in many EU countries the share of renewables and nuclear energy has increased significantly;

-

domestic enterprises have lower automation and energy efficiency in their production processes.

If the same CO₂ price is set for Ukraine and the EU, Ukrainian companies will pay more per tonne of product since they emit more per unit of output. The result is that domestic business automatically becomes less competitive.

6. Export-oriented economy

The price of export products is formed on the global market, not within the country. Domestic enterprises cannot simply pass on higher costs to domestic consumers. As a result, their profit shrinks or disappears entirely.

Under wartime conditions, this is critical, because exports are a source of foreign currency revenue that supports the balance of payments, the exchange rate of the hryvnia, and the budget.

Top 7 problems with the environmental tax in Ukraine

Officials, experts, and analysts point to a number of fundamental difficulties with environmental taxation in Ukraine and the challenges associated with it. A brief overview is provided in the infographic, with more details below.

1. Misallocation and Inefficient Distribution Scheme of Revenues

This is the first issue cited by specialists and business representatives at events dedicated to the “green” transition, as well as in their comments to our publication on this topic.

A significant portion of funds (45%) is allocated to the general fund of the state budget and lacks targeted use. In other words, these payments serve a purely fiscal function rather than an environmental one.

“Reform efforts should first focus on the efficient allocation of funds between the regions and central government,” says Stanislav Zinchenko.

Experts emphasize that such a system leads to the dissipation of funds within the budget and undermines the environmental protection function of the tax. Enterprises lose financial resources that could be directed towards decarbonizing production.

This view is also shared by the National Association of Extractive Industries of Ukraine (NAEIU). Its founder, Kseniia Orynchak, told EcoPolicy:

“In Ukraine, unlike in the EU, the environmental tax is mainly fiscal in nature and does not function as a financial instrument to support and encourage the implementation of environmental measures or enterprise modernization. Funds are dispersed in the general budget fund and do not return to industry as investments in clean technologies. As a result, enterprises lose financial resources that could be used for modernization, enhancing energy efficiency, and implementing low-carbon solutions. Under such circumstances, the CO₂ tax does not accelerate environmental modernization or decarbonization but actually delays it, since it limits opportunities for capital investment in emission reductions.”

2. Flawed Design

Experts point out the necessity to broaden the tax base. Environmental taxes should include those such as royalty payments for the use of natural resources and excises on fuel and vehicles.

This approach exists in the EU, as these types of activities are associated with negative environmental impacts. Accordingly, it makes sense to allocate revenues from these sources to improving the natural environment.

The NAEIU proposes to establish a carbon burden level commensurate with the scale of the national economy and high defense spending amid ongoing military risks, as well as to allow emitters to offset up to 90–100% of CO₂ liabilities by crediting investments in decarbonization and/or modernization projects. At the same time, they suggest eliminating taxation of greenhouse gas emissions for enterprises that purchase quotas from the National Emissions Trading System.

3. Complex administration, information gaps, ineffective monitoring of compliance with standards and tax payments

The Tax Code provides a procedure for calculating the amount of the environmental tax based on emissions data; however, there is no clear methodology for determining these volumes. As a result, enterprises often estimate emissions by eye or even deliberately understate them so that the tax amount turns out lower. Consequently, budgets are deprived of funds.

Only specialists can verify whether an enterprise determines emission volumes correctly. At present, they are physically unable to monitor all taxpayers, especially under the conditions of full-scale war.

4. Lack of incentives for enterprise eco-modernization

In many developed countries, environmental taxes are combined with incentive measures (tax exemptions, grants, subsidies). However, there are no such instruments in Ukraine.

5. Inefficient use of funds

This point deserves a separate article entitled “How to Patch Budget Holes at the Expense of the Environment.” EcoPolicy regularly monitors how Ukrainian communities spend finances that should be allocated for environmental protection measures.

When analyzing the environmental expenditures of local councils, we constantly encounter the substitution of concepts, and funds from the environmental tax are allocated for housing and utility expenses. Communities often direct the environmental tax to pseudo-environmental projects: tree pruning, street cleaning, or patching up pipes under the guise of pollution prevention.

For example, in the Ivano-Frankivsk region, deputies used the war as a pretext for misusing the environmental tax. By the end of 2024, they allocated UAH 6 million of these revenues to implement defense and mobilization programs, as well as for the regional hospital for war veterans.

The head of the ESG Liga Association of Environmental Professionals (PAEW), Olha Semkiv, explains that the effectiveness of environmental tax fund use directly depends on the existence of a system for analyzing, assessing, and tracking the outcomes of their use.

“There are currently insufficient instruments for this. It complicates the understanding of what results are being achieved both at the national and regional levels,” she stated.

The expert noted that the problem lies not only in limited transparency but also in approaches to spending planning. According to her, the current system largely focuses on a list of permitted environmental measures rather than on evaluating their actual environmental effect.

“Under such conditions, financing is not always linked to achieving measurable results in environmental protection,” the expert added.

6. Symptomatic implementation of environmental taxation instruments instead of thorough system reform

“In practice, introducing additional fiscal changes without comprehensively improving the waste management system creates the impression of increased tax pressure without the formation of real environmental instruments. This approach does not meet the principle of proportionality, EU practice, or the task of legislative harmonization,” says Kseniia Orynchak.

Stanislav Zinchenko also recalled:

“Past experience in Ukraine has shown that simply increasing the environmental tax does not solve any issues.”

7. Uniform punitive approach to all sectors without considering their specifics

“Mining industry waste is objectively proportional to the volume of extracted minerals and cannot be reduced through managerial decisions without cutting extraction itself. Thus, the fiscal instrument becomes solely an additional financial burden,” explains the founder of NAEIU.

She draws attention to the fact that EU law, in particular Directive 2006/21/EC, provides for a different approach-the introduction of a financial guarantee (financial security) mechanism. Its purpose is to cover the costs of reclamation and fulfill obligations after the closure of a waste disposal facility.

“Such an instrument is compensatory rather than fiscal in nature and aims to ensure environmental safety, not to replenish the budget,” says Kseniia Orynchak.

What should the architecture of an environmental taxation system look like to promote eco-modernization and improve environmental conditions?

The problems are clear. So what solutions do experts propose?

First and foremost, the experts agree that the entire amount of the environmental tax should be used for its intended purpose. This basic principle, which forms the foundation of the European environmental taxation system, is strongly recommended for implementation in Ukraine as well.

It is necessary to stop viewing the environmental tax as a source of budget revenue. The full amount should be allocated to initiatives that are guaranteed to improve the state of the environment.

It is critically important to develop a mechanism that allows enterprises to use accrued environmental taxes for their own eco-modernization projects, rather than sending them to the general state budget fund.

“EU ETS revenues are earmarked specifically for the needs of the ‘green’ transition. In fact, the EU ETS is not only a tool that creates financial pressure on emitters, but also a means of accumulating financial resources for decarbonization needs,” affirm the experts of GMK Center.

Expert Stanislav Zinchenko also stressed that the targeted use of environmental taxes is a key issue.

“There are growing questions about this, both at the local level and at the State Energy Efficiency Fund. In my opinion, it appears inappropriate when the tax is paid in one region, but then, through the Fund, is used in a completely different one,” he emphasized.

NAEIU proposes introducing the principle of targeted reinvestment. According to this principle, 70–90% of the accrued environmental tax amount, including the CO₂ tax (if an Emissions Trading System is implemented-the cost of quotas), should remain at the disposal of the enterprise provided these funds are allocated exclusively to verified projects on decarbonization, environmental modernization, emission reduction, and the deployment of the best available technologies.

“The point is not about granting privileges or exemption from responsibility, but about transforming the tax into a climate investment fund at the level of enterprises that are directly responsible for emissions,” says Kseniia Orynchak.

В The Association is confident that this approach will enable a dual effect:

- on the one hand, to ensure real and measurable emission reductions;

- on the other – to accelerate the technological modernization of Ukrainian industry in accordance with European climate standards.

Some experts suggest creating a separate body to ensure the targeted and efficient use of environmental funds.

“In my opinion, the main principle of reforming the environmental tax system should be as follows: Ukraine should implement the same 'green' regulations as the EU. That is, our system should be focused not on collecting and redistributing taxes, but on reducing pollution. One of the best instruments could be compensation of investment project costs that reduce environmental impact from the environmental tax payments made by the enterprise,” says Stanislav Zinchenko.

2. Strict control over how the collected environmental tax funds are spent

Cases when communities use these revenues to repair sewage pipes, update municipal vehicle fleets, equip dog walking areas, or even conduct mobilization work should become a thing of the past.

“The architecture of the environmental tax system should be transparent and focused on achieving specific environmental outcomes. The government's role is to establish clear rules and make decisions taking into account the positions of stakeholders and the long-term impact of projects on the environment and territorial development,” says Olha Semkiv.

The expert notes that funding for environmental initiatives-whether grants for business environmental measures or land management projects for nature reserve fund areas (NRFA)-should be based on an open methodology for assessing effectiveness.

“This approach will allow allocating environmental tax funds to actions that achieve real reduction of environmental risks and improvements in the state of the environment,” she explains.

Specialists also propose:

-

To develop a new logic for forming the list of environmental protection measures and enshrine it at the legislative level.

-

Systematically analyze the use of environmental tax funds by central executive authorities and local self-government bodies.

-

To establish liability for misuse of funds.

3. Introduction of new incentives

In their policy brief “Application of Environmental Taxes in Ukraine,” experts from the Centre for Economic Strategy note:

“According to European experience, the environmental taxation system should be combined with incentive measures that will facilitate the transition to a carbon-free economy. These measures may include the introduction of a tax credit system (reducing a company's tax liability by granting a tax discount following environmental transformation) and the creation of financial instruments for businesses aimed at implementing more sustainable technologies.”

4. Gradual increase of the environmental tax to a level comparable with European environmental fees, so that businesses have time to adapt and modernize their production facilities.

“A sharp rise in CO₂ prices will not stimulate the development of the 'green' industry, but, on the contrary, will lead to the deindustrialization of the economy,” experts at GMK Center warn.

Experts also recommend increasing the percentage of rent for the use of natural resources and including a share of this rent in the environmental tax.

5. Step-by-step launch of the national ETS, as closely aligned in architecture as possible to the European EU ETS, and cancellation of the carbon tax for sectors covered by it.

6. The decarbonization fund must live up to its name and provide preferential loans for enterprise decarbonization projects, rather than using the available resources mainly to improve the energy efficiency of the public sector.

7. Transformation of the environmental tax on CO₂ emissions by replacing the direct tax with a tax on the use of energy resources based on the European model or by introducing excise taxes on natural gas, coal, and other energy resources used by households, industry, and public utilities.

8. Improving the administration of the environmental tax system and information exchange between the State Environmental Inspectorate and tax authorities.

The environmental tax in Ukraine requires comprehensive reform: from changing the tax base and strengthening oversight to creating a transparent mechanism for the distribution and use of funds that would ensure real financing of environmental protection measures, rather than patching budget gaps or covering the needs of the housing and utilities sector.