Rechargeable batteries are gradually becoming a fundamental component of the modern economy. Electric cars, energy storage facilities, portable gadgets, drones—these sectors are completely dependent on batteries. In 2025, low prices drove the lithium-ion battery market to grow by 20%, reaching a record $150 billion. However, this balance is very fragile due to the concentration of production and supply chains.

This is evidenced by a report from the International Energy Agency (IEA).

The main "consumers" are electric cars and clean energy

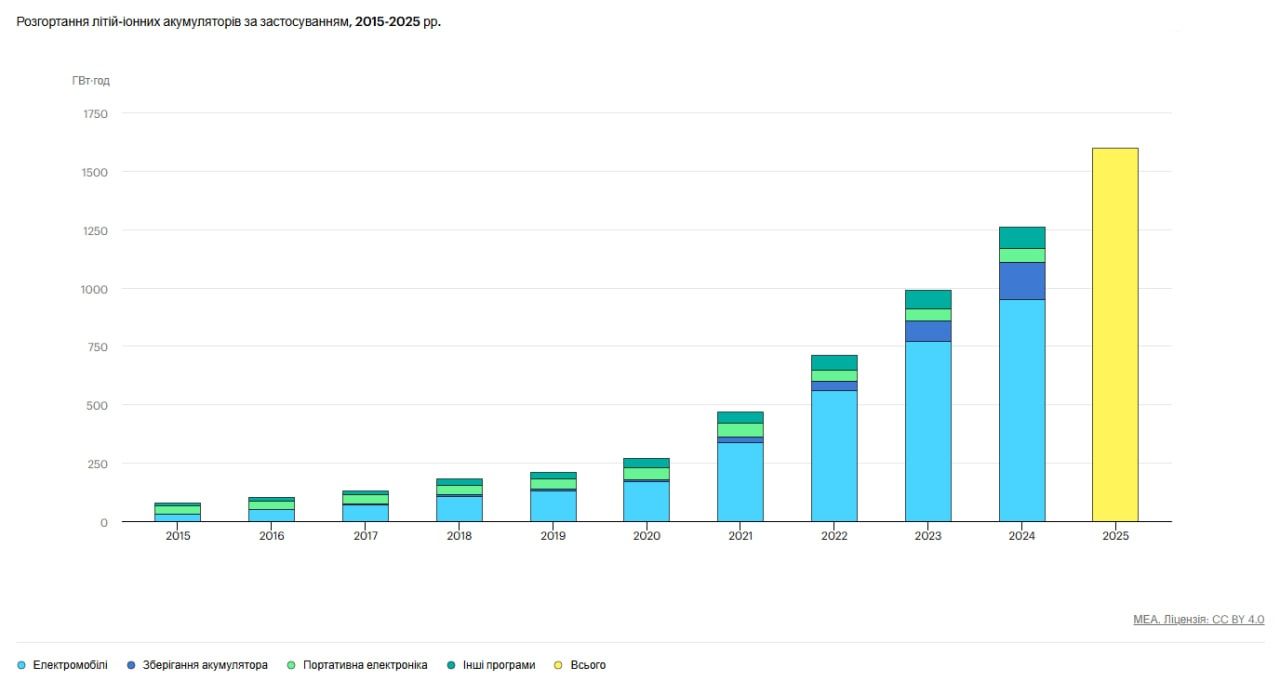

In just five years, from 2020 to 2025, the use of lithium-ion batteries has increased sixfold. Key demand is observed in the following sectors:

Electric transport – 70%. This sector is the main driver of battery demand, as electric vehicle sales keep breaking their own records. According to IEA data, currently every fourth car sold is electric.

Energy storage systems (ESS) – over 15%. Batteries play an important role in stabilising “green” energy grids since solar and wind farms operate unevenly due to weather conditions.

Portable electronics – less than 5%. This sector has seen the largest shift in battery consumption – just ten years ago, it accounted for more than 50% of all manufactured batteries.

Source: International Energy Agency

Decisive factor – price

The battery market’s growth has been primarily driven by the decrease in prices. In 2025, prices dropped by an average of 8%. Several factors contributed to this:

- production innovations;

- improvement of battery chemistry;

- intensification of global competition.

The greatest decrease was observed in the energy storage battery segment. In 2025, average global prices stood at just a third of their 2020 levels.

There are also regional differences in battery costs. Prices were lowest in China, where they were 35% lower than in the European Union and 30% lower than in the United States.

Lithium iron phosphate (LFP) batteries became 15% cheaper, while lithium nickel cobalt manganese oxide (NMC) batteries dropped in price by less than 5%. Therefore, demand for LFP batteries was higher – over 50% for electric vehicles and over 90% for ESS.

However, the IEA notes that the LFP situation is quite unstable – manufacturers, concentrated mainly in China, are operating at a loss.

Energy storage

Over the past five years, the total capacity of global energy storage systems has increased more than twentyfold. This was mainly driven by lower prices, convenient logistics, and relatively fast project implementation rates. ESS are becoming a critical component in green energy markets, which are rapidly developing worldwide.

But here, too, there is dependence on China – over 90% of ESS batteries are LFP type, produced almost exclusively in the People’s Republic of China. Other countries cannot compete with such low-cost products.

Strategic risks

MEA analysts emphasize that global energy systems are becoming increasingly dependent on batteries and, consequently, on their manufacturers. These are mainly China, South Korea, and Japan.

Existing battery manufacturing plants in the EU and the US import most of their components from China. Therefore, a disruption in the supply chain is a global risk. The world needs to diversify battery production, but experts believe that this imbalance is unlikely to change in the near future.

The main reason is the cost of production—in China, it is already well-established and efficient, making it twice as cheap as in the US and Europe.

EcoPolitic previously reported that falling battery prices have accelerated the development of combined energy projects. These involve generating energy from the sun or wind and storing it in battery systems.